(65) 6793 7805

(65) 6793 7805

The reason is partially psychological. Whenever transactions is broken down towards five or higher brief payments because these attributes manage, customers key themselves on the considering these include saving money. You realize the shoes costs $150, like, but due to the fact expenses states $, your rationalize you only have to shell out this much for now.

“This type of preparations reduce the present price of what exactly we have been to get. Future losses usually check reduced terrifying than simply current of those therefore always thought we will be better from the next day,” says Carrie Rattle, a financial therapist which focuses primarily on overshopping. “They use consumers’ overconfidence down the road and impact that we manage to handle the difficulty once the fee appears to be lower amounts.”

One key difference in playing cards and you can BNPL preparations that does let curtail loans buildup: Whenever people are not able to build a repayment or pay completely, they cannot utilize the services once again up until they actually do very. Having said that, because the a lot of companies cannot would borrowing checks or express facts that have most other lenders, customers can just only turn to most other BNPL businesses for brand new borrowing from the bank and possess many of these loans outstanding on top of that.

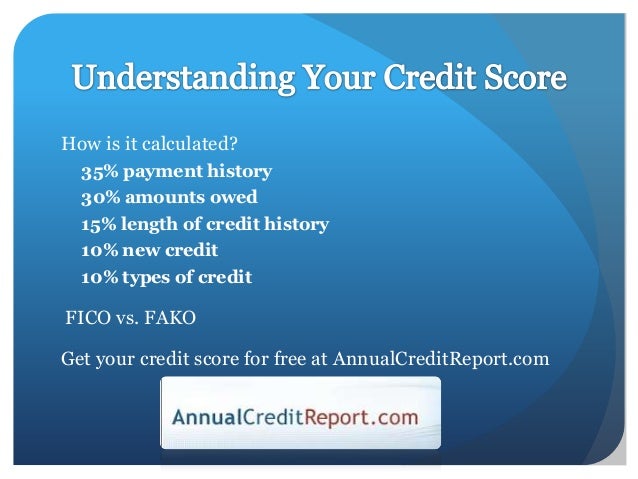

Credit scoring check my reference activities, such as those run of the FICO and you may VantageScore, will additionally must adjust, because the the current formula penalizes people in order to have multiple the latest credit concerns inside a short span of your time and advantages stretched loan-terminology

Now that BNPL plans have left main-stream, credit agencies want it financing guidance most readily useful reflected when you look at the credit reports and are earnestly focusing on taking one to on. Others two significant credit bureaus, Experian and you may TransUnion, also have said they’ll certainly be including more BNPL study so you can its credit history.

Equifax states this will help to lenders top decide whether or not to open this new personal lines of credit to customers, while also satisfying BNPL profiles for their an excellent installment background-a change that may raise mans FICO credit rating, on average, thirteen items to 21 facts.

“Now their borrowing from the bank is not actually affected by BNPL arrangements, if you do not miss a cost otherwise your debt is sent so you’re able to collections,” says Francis Creighton, president and you will Chief executive officer of the Individual Studies Industry Association. “We think this might be difficult. When you do spend on time there is nothing claimed. “

“If you use BNPL functions, you may have seven loans at any single. So you can old-fashioned credit scoring, so it turns out 7 brand new loan requests yet its alot more comparable to seven charges for the credit cards,” claims Creighton. “We should instead guarantee that that is modified accurately so someone utilizing the device due to the fact designed aren’t getting dinged getting starting that which you correct.”

Equifax, as an instance, announced inside December, this do standardize a method to possess revealing these types of financing and begin adding such as study so you’re able to consumers’ borrowing from the bank data probably that it spring season

Get now, pay after agreements would be a good economic tool to aid you pay for necessary, however, large-rates products, particularly if you nab a no % interest rate render. Along with laws and regulations encompassing just how credit bureaus eliminate these types of fund switching, they’re able to also be a smart way to build your borrowing records that have faster chance soon.

Still, as with all forms of borrowing, it is essential to make sure you understand the full terms of your own loan ahead of agreeing and you may feel comfortable conference the desired repayments in light of your own almost every other lingering costs, particularly rent, mortgage payments or education loan costs.

As BNPL money go after their unique plan you to definitely commences towards day of you buy, set-up automatic money and you can commit to receive reminders regarding the after that expense. This way you simply will not need to monitor numerous repayments. Just be sure you have got enough on your membership when these services need an automated commission or you might feel strike that have good $thirty five overdraft fee from your own bank.